Venture Debt is a short to medium term debt which is designed as per the need of a start up during their growth phase. Start-ups who had raised Equity funding from Angel or Seed or Venture Capital investors are preferred by Venture Debt Investors as an alternative funding option.

Venture Debt Investors first understand the start-up’s unique business model and their funding requirement in their early stage of the business and based on the venture’s cash-flow projections, they structure the terms of the debt. Start up with their initial years of building the business ending up in losses, will find it difficult to raise traditional bank funding. In addition, most start-up ventures are with asset light business models leaving no physical assets to hypothecate as security which is the primary demand by the banks for funding. Generally, Venture debts do not require any cash collateral, pledge of equity shares or personal guarantees but such Investors may demand hypothecation of the Brand or IP in their favour.

Another important feature is that the promoters and early stage investors dilute nominally when they raise venture debt. It is one of the financing option to augment the growth with minimal equity dilution and at a cost less than the cost of equity.

Another important feature is that the promoters and early stage investors dilute nominally when they raise venture debt. It is one of the financing option to augment the growth with minimal equity dilution and at a cost less than the cost of equity.

Venture debt over the last decade has become popular in India. The active funds in this space include Alteria capital, Innoven capital and Trifecta capital. These investors are mostly registered as domestic entities though they have been incorporated by non-resident Investors in compliance with Indian regulatory requirement.

Start-ups like Bigbasket, Curefit, , Dunzo, Lendingcart and Ninjacart have availed Venture Debt. Over 2500 crs have been deployed as venture debt in the last few years. Most of the Venture Debt Investors are active in Ecommerce, Edutech, Healthcare, Mobility, Food Tech and Fin Tech sectors.

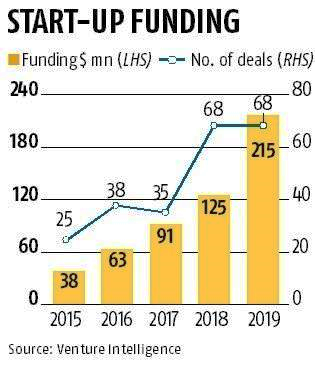

As per Venture Intelligence over USD 215 million is invested as Venture Debt in 2019 over 68 deals.

Venture debts are issued in various forms like term loans, receivable financing, short term working capital on project based, with repayment terms in the form of monthly pay-out post a minimum moratorium period or a bullet payment at the end of the tenor or bill to bill repayment based on the business model of the company and the need of the start up. An equity conversion with a right to subscribe to shares in future funding may be a precondition for some of the deals.

Venture debts are issued in various forms like term loans, receivable financing, short term working capital on project based, with repayment terms in the form of monthly pay-out post a minimum moratorium period or a bullet payment at the end of the tenor or bill to bill repayment based on the business model of the company and the need of the start up. An equity conversion with a right to subscribe to shares in future funding may be a precondition for some of the deals.

The tenor of the loan ranges from 2 to 3 years and the coupon rate is marginally higher than the rates offered by NBFCs, since the risk involved in offering debt to Start-ups is significantly higher.

Like Equity investments, the funds go through a proper due diligence of the start up before sanctioning the facility. The venture debt investors will execute a standard agreement with rights and covenants including creation of security if any. Generally, they do not insist on a board representation for the facility except in the case of an event of default.

The vacuum created by the market in terms of debt funding from traditional bankers/NBFC has given an opportunity for an alternate funding for the start up in the form of venture debt. Start up can raise midterm growth capital from venture debt investors with minimal equity dilution. It is a boon for the start-up who had raised equity funding earlier from structured Investors to scale their business faster and achieve a higher valuation for the next round of funding with venture debt.

This alternate funding option for start-up is becoming extremely popular in the last few months with more and more VCs offering this facility.

No comment